Interest Rates on the Rise, But Markets Hold Gains

Presented by Tim Weller

As we head toward the end of February, the big picture is still positive—but the risks may be on the rise. Specifically, the improvement has slowed or reversed for new cases, positive testing rates, and hospitalizations. It’s too early to worry about a full reversal, but some risk factors appear to be coming into play.

Part of the slowing improvement is likely from reopening effects. The other significant risk is that a more contagious variant of the virus is accelerating infection growth, as it has in other countries. We don’t know yet which is the primary driver. Another factor that may be slowing improvement is that progress in vaccinations has slowed, with a combination of bad weather and distribution problems.

The economic news is doing better. The federal stimulus bill has improved both confidence and spending, with personal consumption strong last month. Reopening in many states has continued, which has helped as jobs were positive in January, and layoffs were down significantly last week. Business spending remains strong. While medical risks remain, the economy looks likely to be able to keep growing.

That continues to be what markets are thinking, as they remain close to all-time highs despite some turbulence. Let’s take a look at the details.

The Virus: Case Growth Ticks Back Up

New cases per day. The most obvious metric for tracking the virus is daily new cases. Case growth remains low by recent standards, now at levels last seen in October and early November, but has recently ticked up again. This may be due to the winter weather, which slowed case reporting, in which case the bump could represent a catch-up. That would be the best-case scenario. The other alternatives are that reopening has started to generate new cases or that a more infectious variant of the virus has started to push infection rates up again. We will not know which is the case for another couple of weeks, and we need to keep an eye on that. So far, however, conditions remain reasonably favorable.

New daily infection rates were 75,299 on February 24, up from 73,945 a week earlier—the first week-on-week increase in some time. The seven-day average number of new cases per day was 70,678, down from 81,033 a week ago, but that number has been ticking up over the past couple of days. Case growth remains too high. While it is down significantly, there is a possibility that the trend could be reversing.

Source: https://www.worldometers.info/coronavirus/country/us/

Source: https://www.worldometers.info/coronavirus/country/us/

Hospitalizations. We also see the same trend with hospitalizations, although not as pronounced. While case reporting has weaknesses in how the data is reported, hospitalizations are much better as a real-time indicator. Here, too, we can see a moderation in the improvement trend. On February 24, there were 54,118 people hospitalized, down from 63,405 a week earlier. As a coincident indicator and as a better indicator of the stress on the health care system, this supports the idea that the trend is still improving, but at a slower rate.

Source: https://covidtracking.com/data/charts/us-currently-hospitalized

Testing news. The news is also mixed on testing, however. While the positive rate continues to decline, so have the overall testing numbers. While daily testing remains at historically high levels, the decline is potentially a risk factor. Nonetheless, the continued decline in the positive testing rates is more supporting evidence for continued improvement and could be a leading indicator of further improvements. Source: Johns Hopkins University

Source: Johns Hopkins University

Vaccinations. Finally, we are now well into the vaccination process. More than 13 percent of the U.S. population has now had at least the first shot of the vaccine, and this has very likely contributed to the positive change in trend in the other data series. While the trend has slowed in the past week, this is likely weather related, and vaccinations have started to grow faster again, which should drive further improvements.

Source: https://ourworldindata.org/covid-vaccinations

The major risk continues to be that a more contagious strain of the virus could take root and accelerate infections again. Here, too, we see no immediate signs of this. But evidence of these strains has now been reported in 35 states, and it could be behind the recent uptick in new cases. So far, there has been limited spread, but this remains a very real risk.

The bottom line is that infection growth is still too high and that the improvements, while real, have paused in recent days. Policy measures appear to be loosening around the country, which may have had an effect, but the real risk is a more infectious strain of the virus. We need to keep an eye on this. Despite that, vaccine deployment continues to moderate the risks. As that accelerates, the downside risks will drop quickly.

The Economy: Damage Is Moderating

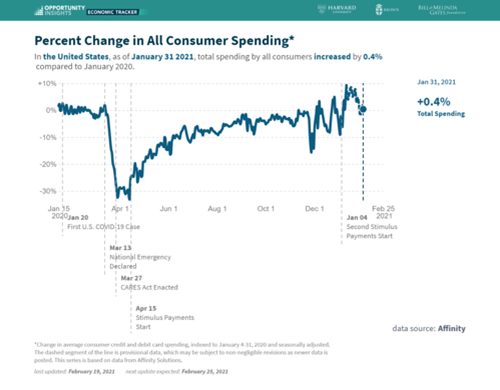

Jobs and consumers. While the backward-looking economic data remains soft, we are seeing improvement in more current indicators as a combination of medical improvement, slow reopening, and the federal stimulus acts to help employment and confidence. Job growth went positive again in January, after declines in December, and layoffs dropped significantly last week. Confidence also seems to be bottoming. While the data is preliminary, the combination of a firming job market and stabilizing confidence appears to have started to grow consumer spending again, as shown by last month’s strong personal spending report. With all of this, the data is showing we are likely through the worst of the economic impact of the pandemic.

Source: https://tracktherecovery.org/

Source: https://tracktherecovery.org/

Business sector. This improvement is also what the business sector is expecting. Despite the slowing in the consumer economy, business investment continues to rise and remain above pre-pandemic levels.

With the improvements in hiring and spending, the consumer economy looks to be past the worst of it and set for further improvement in coming months. The business economy was already solid and looks to be improving even further. As the stress lifts, with the existing and prospective fiscal stimulus package, the economy now looks like it can continue to keep growing even if the medical improvements slow. While the risks are real, we now see most of the economic risks are moving behind us as well.

The Markets: Hold Gains Despite Rising Interest Rates

Markets saw some volatility last week, largely attributed to increases in interest rates. But this, too, represents progress, as that increase is based on continued economic improvement. Despite that turbulence, between the ongoing medical and economic improvements, markets continue to expect a much better 2021, and that has supported prices. Fourth-quarter earnings are coming in well ahead of expectations. Further, analysts are now adjusting their 2021 earnings estimates upwards, which suggests this positive trend might continue as well.

The Long View

While conditions remain favorable by recent standards, the pause in medical improvement suggests that medical risks may be on the rise again. It is too early to be certain but not too early to pay attention. Offsetting that, with economies reopening and the federal stimulus supporting the most vulnerable parts of the economy, the economy continues to improve. Markets will likely keep bouncing around on new developments, so expect more volatility in the short term.

In the longer term, the good news is that vaccines are now rolling out increasingly quickly. In a couple of months, we should be approaching the end of the pandemic when the economy can normalize and start to really grow again. Despite the real risks that still remain and the possibility of a medical setback, we are making progress.

Weller Group is located at 6206 Slocum Road, Ontario, NY 14519 and can be reached at 315-524-8000. Securities and Advisory Services offered through Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services serviced through Weller Group LLC and KAFL, Inc. are separate and unrelated to Commonwealth.

Authored by Brad McMillan, CFA®, CAIA, MAI, managing principal, chief investment officer, at Commonwealth Financial Network®.

© 2021 Commonwealth Financial Network®